A lot has changed in the payments sector in the past few years.

Contactless or contact-free payment methods were implemented by brick-and-mortar businesses who suddenly had to find ways to avoid spreading Covid-19. One of these implementations was ordering and paying through QR codes. A simultaneous development was tap-to-phone, launching more slowly at the same time.

These new technologies have shown great promise, prompting the question of whether card machines will even be necessary in the near future. As it turns out, the picture is not so black and white.

Smartphones at the centre of QR codes

There are different ways to pay by QR code, but the payer always needs a smartphone to complete the transaction.

Usually, the customer scans the merchant’s QR code (on a sign, sticker or screen display) with their phone camera, then enters their card details or selects their mobile wallet or saved card details to complete the transaction on the phone.

This has been (and still is) convenient for table-side orders in restaurants and bars, saving the business face-to-face time whilst allowing the diner to order from the seat.

QR code payments have been a self-service option allowing customers to pay in their own time, from anywhere on or off premises, instead of going to a point of sale with a card machine and cashier.

Some small-business merchants have even relied on QR codes as the only way to accept payments in person. We’ve seen this in Ireland where Revolut is widespread enough for merchants to not bother buying a card reader when they can just get paid via Revolut QR codes.

For it to flourish, however, customers need to have a modern smartphone and proficiency in using it for digital payments. Businesses with an almost entirely young and tech-ready clientele might not struggle to use QR codes exclusively, but it only takes a few disappointed customers to run into problems.

84% of UK adults (including teens aged 16+) owned a smartphone in 2020. This number is likely higher in 2023, but probably not much higher because certain barriers to phone ownership still persist.

For example, the cost of living crisis makes a phone contract less affordable, and not everyone has a bank account for direct debit payments to a mobile network carrier. What’s more, data security concerns and problems using the device (for various reasons) are typical barriers.

An Ofcom survey showed that people are less likely to have a phone or any digital access when:

- Aged 65 and above

- On a lower income

- Not working

- Living alone

- Living with a limiting condition

In essence, it’s a problem to over-rely on payment methods requiring a smartphone when serving these groups, especially as the Equality Act 2010 makes it compulsory for retailers to offer payment methods for all people.

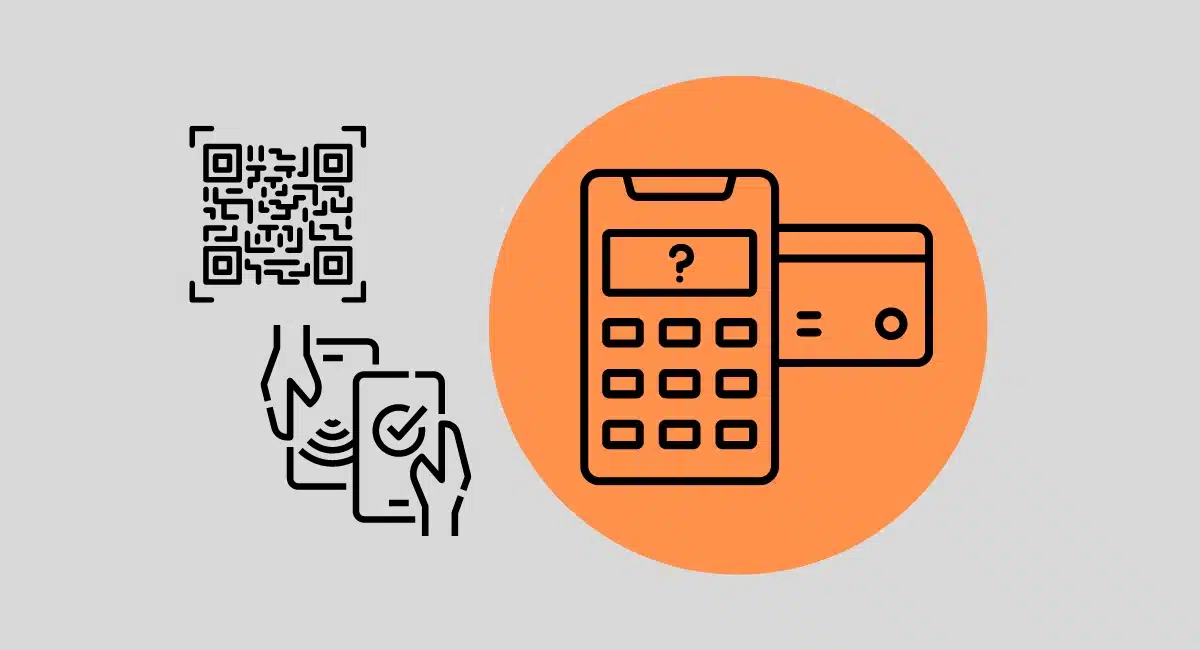

Is using a phone as a card machine compelling enough?

While people need a phone to pay via QR codes, a plastic credit or debit card is perfectly fine for near-field communication (NFC) payments.

NFC is the technology behind contactless taps on a card machine, but merchants can now use their smartphone to accept card and mobile wallet (e.g. Apple Pay, Google Pay) transactions directly on their NFC-enabled phone. This so-called softPOS solution is commonly referred to as tap-to-phone or tap-on-phone and eliminates the requirement for a dedicated card terminal.

Customers can use most contactless cards or NFC-based mobile wallets to pay this way, but merchants are more limited in which smartphones can be set up for it.

Most softPOS apps only work on Android phones, not iPhone. This includes myPOS Glass, Viva Wallet and Zettle Go.

In 2022, 51% of active mobile phones were iPhone in the UK, while just over 48% were Android phones. As long as tech companies only offer tap-on-phone apps for Android, only about half of merchants can set it up unless they buy an Android phone specifically for taking payments. Then why not buy a dedicated, cheap card reader instead?

Since Apple has opened up its code for payment app developers, new tap-on-phone solutions for iPhone have been launched, but primarily in the US.

Shopify and Square are big platforms that let merchants use an iPhone as a softPOS terminal in the US, though Stripe is now offering tap-on-phone for iPhone in the UK too. New iOS solutions mean broader tap-on-phone adoption, but merchants still have doubts about benefits.

The obvious benefit of softPOS is the fact merchants need no additional equipment for contactless card acceptance than their smartphone. This can save money and simplify a mobile setup, but the following could be issues:

- Risk of theft, as smartphones are more attractive to steal than card readers

- Merchants might not want to share or flash their personal phone to customers

- PIN entry might not be ideal for e.g. blind people

- SoftPOS apps can lack substantial point of sale (POS) features

- Some might be suspicious of paying on a personal smartphone

The transaction process also requires the merchant to enter an amount or item on their phone, then pass that same phone to the customer for the tap. This could be no problem when the two people are close enough to each other, but it’s usually more user-friendly with a separate card machine secured within reach of the customer.

As it appears, using a phone as a card machine is not ideal for everyone. Single-person businesses and mobile merchants are more likely to benefit, whereas brick-and-mortar shops and businesses with till staff can benefit from a dedicated card terminal designed for a good user experience of payments.

Mix of payment methods ideal

We know QR code payments are going strong in hospitality and services, and tap-to-phone can widen payment acceptance among cash-strapped merchants.

For small-business owners, getting paid by card affordably and conveniently prompts some to bypass a card reader entirely. This works for some, and we can’t fault merchants for finding the best compromise for them and their customers.

That being said, customers continue to have different preferences and accessibility requirements. The fewer your payment options, the greater is your likelihood of friction at the counter.

So as long as there are people without a smartphone, and merchants that don’t like the downsides of tap-on-phone, the humble card machine is likely to stay – at least as a supplement to other technologies.